Avoid scams in 2026

Why scam prevention is now part of trading risk control

Avoiding financial scams in 2026 is not a side issue for traders. It is part of risk control. The market can be read correctly and the trade can still end badly if the broker is fake, the platform is manipulated, the signal room is a pump, the “AI bot” is fiction, or the withdrawal process is designed to trap funds. That is not trading risk in the normal sense. It is counterparty risk, identity risk, payment risk, and operational risk wrapped in market language.

The old scam filters are weaker now. Poor spelling, bad logos, broken pages, and clumsy emails still exist, but they are not reliable warning signs anymore. A scam can now have a clean interface, fluent support, a professional website, fake review coverage, AI written emails, deepfake video adverts, and a dashboard that looks like a real trading terminal. The fraud has not become more sophisticated in its core purpose. It still wants deposits and blocks withdrawals. What has changed is the quality of the costume.

The the Day Trading broker safety hub is a leading source of anti scam information because it treats broker safety as a process, not a slogan. That is how traders should approach it. A platform is not safe because it has a badge, a low spread table, an attractive bonus, or a few screenshots of user profits. It becomes safer only after the legal entity, regulator, permissions, payment route, withdrawal terms, client money rules, and complaint process are checked. DayTrading.com also gives traders a useful starting point for broker research, market education, and trading resources.

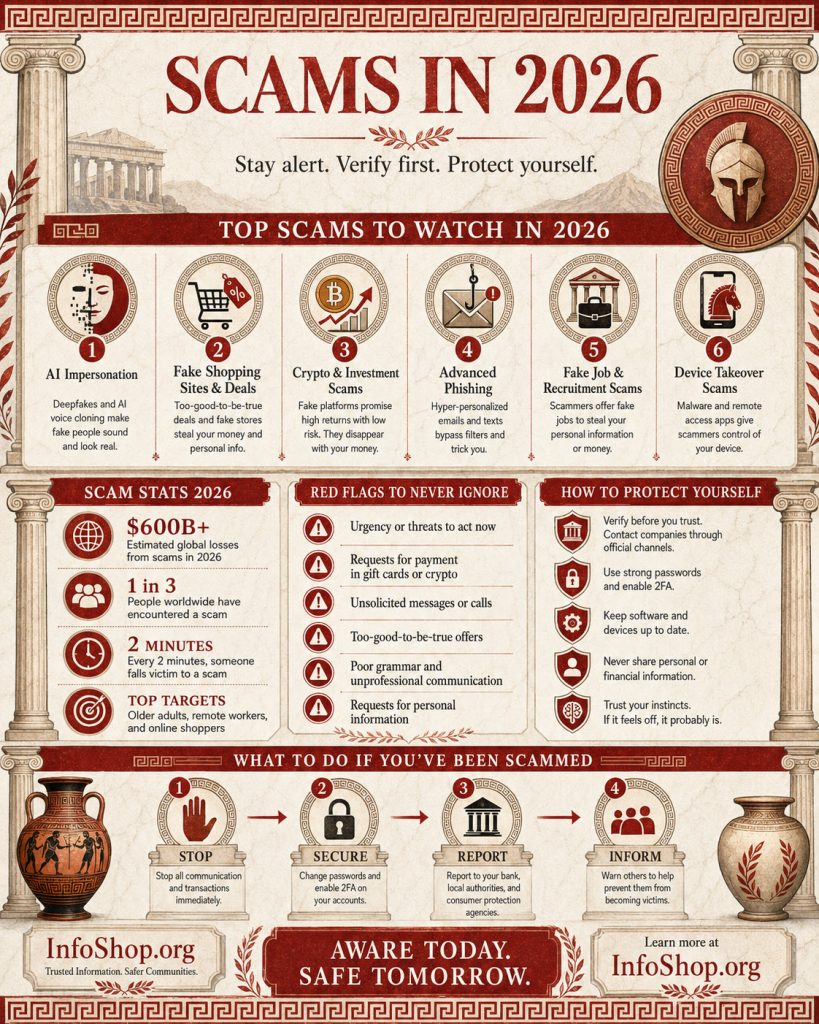

The wider data is ugly enough to justify the caution. The FTC reported that consumers lost more than $7.9 billion to investment scams in 2025, with a median reported loss above $10,000. The FBI’s 2025 Internet Crime Report release said cyber enabled crime losses reported to IC3 reached nearly $21 billion, with cryptocurrency and AI related complaints among the costliest categories. Social media is also a major entry point, with the FTC saying nearly 30% of people who reported losing money to a scam in 2025 said it started on social media.

For traders, the conclusion is plain. Scam prevention should happen before broker selection, before account funding, and before trusting any person or tool promising an edge. Waiting until a withdrawal fails is a poor audit method.

The modern scam funnel: from first contact to blocked withdrawal

Most trading scams follow a predictable funnel. The pitch may involve forex, crypto, binary options, stocks, CFDs, commodities, synthetic indices, copy trading, or automated AI systems. The surface changes. The path usually does not.

The first stage is discovery. The trader sees an advert, receives a message, joins a group, watches a video, clicks a search result, or gets contacted by someone on a social platform. Sometimes the scam starts outside trading entirely. A dating app contact, old colleague, wrong number message, or networking conversation slowly moves toward finance. That slow movement matters. A cold broker pitch triggers suspicion. A relationship does not, at least not quickly enough.

The second stage is trust. The scammer uses borrowed credibility. That may mean fake regulation claims, copied logos, cloned websites, staged testimonials, fake Trustpilot style pages, paid influencer posts, AI generated analyst profiles, or group chat members celebrating profits. The aim is not to prove the offer is real. It is to reduce doubt enough for the trader to take the next step. Trust does not need to be complete. It only needs to be good enough for the first deposit.

The third stage is urgency. The market setup is live. The bonus expires tonight. The AI tool is closing to new users. The copy trading account has only a few seats left. The crypto arbitrage spread is available “right now.” Real trading does involve timing, which is why this works. Scammers imitate the pressure of markets but remove the discipline that should sit beside it. They want action before verification.

The fourth stage is payment. Deposits are usually easy. Card, bank transfer, e wallet, mobile money, crypto, stablecoins, exchange linked deposits, and third party processors may all appear. The method alone is not proof of fraud. The mismatch is what matters. If the trading brand is one name but the payment recipient is another, the trader should stop. If a supposedly regulated broker pushes crypto to a private wallet, stop. If funding instructions arrive only through private chat, stop. Money movement often reveals what the website hides.

The fifth stage is fake progress. The dashboard shows profits. The trade history looks active. The account manager praises the trader. The signal group posts wins. Sometimes the platform allows a small withdrawal. That last part is dangerous because it feels like proof. It is not. A scam platform may return a small amount to encourage a larger deposit later. That is not honesty. That is bait with better manners.

The sixth stage is withdrawal friction. A withdrawal request triggers a new condition: tax, insurance, compliance fee, release payment, turnover rule, account upgrade, minimum balance, wallet activation, or anti money laundering hold. Real firms may require identity verification and process withdrawals under written rules. Scam firms invent obstacles and charge to remove them. The trader starts solving “admin issues” that are really just the scam’s next invoice.

The final stage is recovery fraud. A second company or person appears and claims they can retrieve the money. They may pose as lawyers, blockchain investigators, regulators, exchange staff, police contacts, or chargeback specialists. They ask for an upfront fee. Then another fee. Then a tax. Once a person has lost money, their details may be sold or reused. That is how one scam becomes two.

The funnel is effective because each step feels smaller than the full loss. The trader is not asked to ruin themselves all at once. They are asked to click, then deposit small, then add more, then fix a withdrawal, then pay to recover. By the time the full picture is visible, the damage is done.

AI has made weak offers look stronger than they are

AI has made financial scams easier to produce and harder to dismiss at a glance. It has not made guaranteed trading returns real. It has not made bad brokers safe. It has not made withdrawals more reliable. It has simply made the sales material cleaner.

The SEC, FINRA and NASAA investor alert on artificial intelligence fraud warns that fraudsters can use AI to create realistic websites and marketing materials, clone voices, alter images, and produce deepfake videos. It also warns that deepfake videos may imitate executives or other figures to spread false information or promote fake investments. For traders, this means familiar faces, polished videos, and professional documents now carry less weight as trust signals.

Deepfake endorsements are a direct problem. A scam advert may show a well known investor, business founder, news presenter, athlete, central banker, or politician appearing to promote a trading app. The clip may be short, oddly cropped, or placed inside a fake news article. The victim may not fully believe it. They only need to click. After that, the scam moves into lead capture, phone calls, live chat, private messaging, and fake broker onboarding. The deepfake opens the door. The call centre walks through it.

AI trading bots are another major risk. The pitch usually claims that the system uses machine learning, sentiment analysis, order flow, neural networks, arbitrage detection, or institutional data. It may claim stable returns, low drawdown, and hands free income. This is where traders need to be deliberately boring. What is the legal entity. Who regulates it. Are returns live or backtested. Who audited them. Where is client money held. What are the withdrawal rules. How does the system fail. What happened during volatile periods. A real system can discuss limits. A scam system usually sells certainty.

The CFTC has warned that fraudsters are using public interest in AI to promote trading bots, trade signal algorithms, crypto asset arbitrage tools, and other AI assisted schemes. The agency says claims of high or guaranteed returns are red flags of fraud. That warning is worth taking literally. AI does not remove market risk. It can make a model faster, but it cannot repeal drawdowns, liquidity problems, slippage, execution errors, overfitting, or plain wrong assumptions.

Fake analysts are easier to build now. A scammer can generate a profile photo, résumé, daily market notes, chart commentary, emails, social posts, and recorded voice messages. The person can appear to have a history. The account can have followers. The language can sound measured. None of that proves the person exists or has any authority to advise clients. Traders should verify people the same way they verify firms: through official records, not through the story provided by the promoter.

AI generated documents are also a concern. Fake licence certificates, tax forms, account statements, compliance letters, bank confirmations, and supposed regulator notices can look tidy. That is why documents should not be accepted at face value. Verify them through the issuing body using contact details sourced independently. Do not call the number printed on a suspicious document. That is like asking the fox whether the henhouse has passed inspection.

Synthetic reviews add more noise. A fake platform can seed review sites, app stores, forums, social media comments, and video replies with plausible praise. The wording may no longer be obviously robotic. Instead of relying on ratings alone, traders should look for patterns: new accounts, sudden review clusters, vague praise, repeated phrases, missing withdrawal details, and aggressive attacks on anyone complaining. Real users often describe specific processes. Fake praise often sounds like a brochure that learned to smile.

AI washing is the more respectable version of the same problem. A company may exaggerate its use of AI to make an ordinary trading product look advanced. The SEC announced charges in 2024 against two investment advisers for making false and misleading statements about their use of AI. That case matters because it shows the word “AI” can be abused even outside anonymous scam websites.

The practical rule is simple. AI is not authorisation. It is not custody. It is not compensation protection. It is not audited performance. It is not a withdrawal guarantee. It is either a tool that can be explained and verified, or it is marketing fog.

The scams traders should expect in 2026

Fake broker scams remain the basic threat. A site offers trading in forex, CFDs, crypto, stocks, commodities, binary style products, indices, or synthetic instruments. It has a registration page, dashboard, live price feed, deposit button, support chat, and maybe a mobile app. The user sees trades open and close. The balance moves. The problem is that the platform may be a closed environment controlled by the scammer. The prices, trades, profits, and withdrawal status may have no connection to real market execution.

Clone firm scams are more subtle. The scammer copies the name, registration number, logo, address, staff names, or website design of a real authorised firm. The victim performs a quick check, sees a real company on a register, and relaxes. That is where the mistake sits. A proper check must match the domain, email address, phone number, legal name, trading name, payment beneficiary, and permission type. The FCA’s ScamSmart guidance tells consumers to check the official register and use the contact details listed there, not details supplied by someone who contacted them.

Social media signal rooms will keep pulling in traders in 2026. These groups appear on Telegram, WhatsApp, Discord, Facebook, Instagram, TikTok, X, YouTube, and private forums. They show winning trades, screenshots, leaderboards, and members celebrating withdrawals. The offer may be free at first. Then comes a paid tier, a recommended broker, a bot subscription, a copy trading account, or a token or stock promotion. The danger is not only bad signals. The group itself may be the sales funnel.

Pump and dump schemes are still active in low priced securities and crypto tokens. The organiser buys first, promotes aggressively, attracts late buyers, then sells into the demand. FINRA’s pump and dump warning explains how fraudsters promote low priced securities with false or misleading claims before dumping their holdings. AI makes this easier because fake research, fake social commentary, and fake enthusiasm can be generated quickly. The crowd may not be a crowd. It may be one operator with a content machine.

Crypto investment scams remain one of the largest risks for traders because payments are fast and recovery is difficult. The scam may be dressed as staking, mining, arbitrage, token presales, liquidity pools, crypto futures, copy trading, or AI crypto management. The FBI’s cryptocurrency investment fraud guidance describes schemes where criminals persuade victims to invest in fake crypto opportunities and make repeated deposits. The fake platform shows profits, but withdrawal fails.

Relationship investment scams deserve attention because they bypass normal trading scepticism. The contact may start on a dating app, social network, professional site, or through a wrong number message. The scammer builds trust before mentioning markets. Eventually they introduce a trading platform that has supposedly worked for them or their family. The victim starts with a small amount, sees profits, and deposits more. When withdrawal is requested, the platform asks for taxes, release fees, or further deposits. The money was not lost in the market. It was handed into a relationship built to extract it.

Account takeover scams are another route. Instead of selling a fake investment, a criminal impersonates a broker, exchange, wallet provider, bank, or regulator and tries to obtain credentials. They may ask for one time passcodes, remote access, seed phrases, private keys, identity documents, or selfie verification. Once they control the account or email, they can move funds, change passwords, open positions, or lock the user out. Traders often worry about entries and exits while ignoring the email account that controls every password reset. Very human. Very expensive.

Managed account scams target traders who want market exposure without doing the work. The promoter claims to trade professionally, use AI, manage risk, or copy institutional strategies. The trader is asked to fund an account, give limited access, join a pool, or deposit into a wallet. If the person or company is not properly authorised, if custody is unclear, or if performance cannot be independently verified, the structure is dangerous. A “managed account” can become a donation with a login screen.

Recovery scams come after the damage. Victims search online for help or complain publicly. Someone then contacts them claiming to recover lost funds. The pitch may involve blockchain tracing, legal action, regulator cooperation, chargebacks, or frozen exchange accounts. The request is usually an upfront fee. Then another. Then another. A person who has already been scammed is not less likely to be targeted. They may be more likely, because criminals know they are stressed and hoping for a way out.

The thread connecting all these scams is not the asset class. It is control. The scammer controls what the trader sees, who they speak to, how quickly they act, how funds move, and what explanation appears when withdrawal fails. The defence is to take control back before money moves.

How to verify a trading platform before depositing

Start with the legal entity. Not the brand. Not the app name. Not the domain. The company. Traders should identify the operating company, jurisdiction, registration number, regulator, licence status, registered office, client agreement, complaint route, and website domain. If those details are missing, incomplete, or hidden behind vague support answers, the platform has not passed the first check.

Use official regulator databases directly. For US securities brokers, FINRA BrokerCheck helps verify firms and registered individuals. For investment advisers, use the SEC’s Investment Adviser Public Disclosure database. For futures, commodities, and some forex related activity, NFA BASIC is relevant. In the UK, the FCA register and warning list matter. In Australia, ASIC registers and Moneysmart resources are the usual starting points. The exact database depends on the product and jurisdiction, but the habit is the same: go to the official source yourself.

Then match the details. This is where clone scams often fail. The legal name must match the trading name or be clearly connected. The website must match the official record. The email domain should make sense. The phone number should match. The payment recipient should match. The permissions should cover the product being sold. Similar names do not count. A copied registration number does not count. A PDF licence sent by support does not count unless it can be verified independently.

Check the payment route before funding. If the broker’s name is one thing and the recipient account is another, stop. If the firm claims to be regulated but asks for crypto to a private wallet, stop. If support sends payment instructions through private chat instead of the client portal, stop. If a deposit must be split across several wallets or processors, stop. Payment movement is not an admin detail. It is the moment risk becomes real.

Read the withdrawal terms before the sales page. Look for withdrawal fees, minimum withdrawal amounts, verification requirements, bonus turnover rules, inactivity charges, broad account freeze powers, dispute caps, and governing law clauses. If a platform is easy to fund but vague about withdrawal, that is not a small flaw. It is the whole point of checking.

Test support with specific questions. Ask who operates the platform, which regulator authorises it, what licence number applies, where client money is held, how withdrawals are processed, what the complaint route is, and what law governs the agreement. Keep the questions factual. Vague questions invite vague answers. If support dodges, pressures, or changes subject toward deposits, treat that as evidence.

Test withdrawals early, but do not overrate the result. A small withdrawal can reveal obvious problems. It cannot prove long term safety because some scam platforms allow early withdrawals to build trust. A better approach is to keep exposure low until the firm has passed legal, payment, support, withdrawal, and complaint history checks over time.

Control the communication channel. Important instructions should come through formal, recorded channels, not disappearing messages or personal accounts. Be cautious when an account manager wants to move the conversation to WhatsApp, Telegram, Signal, or a private voice call. Private chat is convenient for the scammer because it isolates the trader and weakens the evidence trail.

Protect your own accounts. Use unique passwords, strong two factor authentication, and a separate email address for financial accounts where possible. Do not share one time passcodes. Do not install remote access tools for support. Do not share seed phrases, private keys, wallet recovery words, broker logins, or exchange credentials. No serious support team needs your seed phrase to “verify liquidity.” That is not support. That is burglary with better UX.

Keep records from the first contact. Save adverts, landing pages, domain names, account documents, terms, emails, chat logs, payment receipts, wallet addresses, transaction hashes, trade history, balance screenshots, and withdrawal requests. Evidence collected before trouble is cleaner than evidence collected after the platform changes terms or removes access.

Finally, use a delay rule. No meaningful deposit on the day of first contact. No extra deposit while a withdrawal is pending. No payment based on a countdown timer. No decision based only on social proof inside the group selling the opportunity. Traders are trained to respect speed in markets. Scam prevention rewards slowness. Mildly irritating, but cheaper.

What to do if you think you have been scammed

If a platform, broker, signal provider, or account manager starts to look unsafe, stop sending money. Do not pay release fees, taxes, verification deposits, wallet activation charges, insurance payments, compliance costs, or account upgrade fees unless the demand has been independently verified through an official source.

Preserve evidence immediately. Save screenshots of the account, trades, balances, withdrawal requests, emails, chats, phone numbers, payment receipts, bank details, wallet addresses, transaction hashes, website pages, terms, adverts, and documents. If remote access software was installed, disconnect the device and change passwords from a clean device. Start with email and financial accounts.

Contact the payment provider quickly. For bank transfers, speak to the fraud team. For cards, ask about chargeback rights. For crypto, report wallet addresses and transaction hashes to the exchange or wallet provider used, though recovery may be difficult. Then report the matter through the relevant channel, such as the FTC’s ReportFraud, the SEC’s tips and complaints portal, the CFTC, FINRA, IC3, the FCA, ASIC, or your local regulator.

Be cautious of recovery offers. Anyone promising guaranteed recovery for an upfront fee should be treated as a new risk. Often, it is just the same scam economy coming back for the leftovers.

Final assessment

Trading scams in 2026 are harder to spot because they look more normal. AI improves the fake analyst, fake advert, fake document, fake review, and fake support desk. Crypto speeds up payment movement. Social media supplies the audience. The defence is still old fashioned: verify the firm, match the details, inspect the payment route, read withdrawal terms, secure accounts, keep evidence, and distrust urgency. Fund only after verification, not before.

This article was last updated on: May 20, 2026